83% of North American Manufacturers Are Likely to Reshore Their Supply Chains in 2021 [Report]

Welcome to Thomas Insights — every day, we publish the latest news and analysis to keep our readers up to date on what’s happening in industry. Sign up here to get the day’s top stories delivered straight to your inbox.

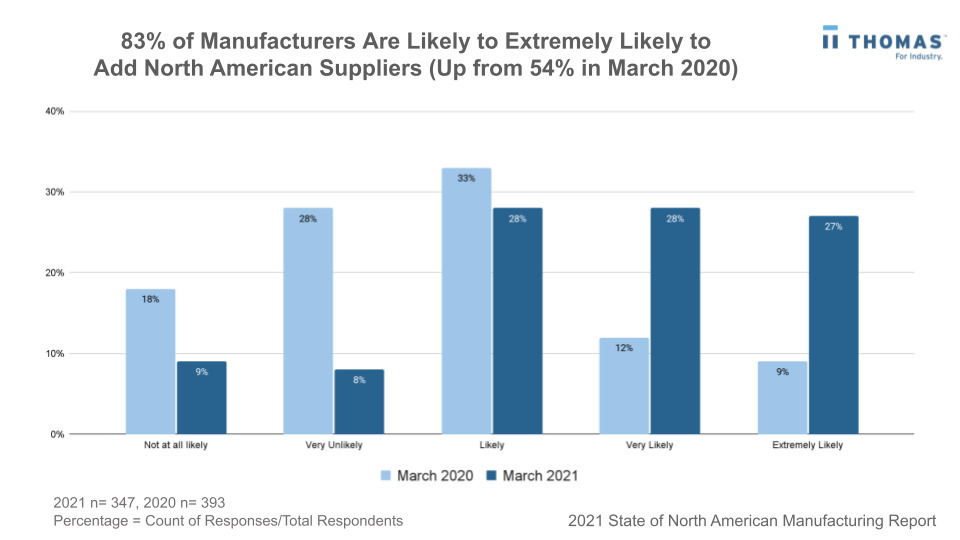

According to the latest 2021 Thomas State of North American Manufacturing Report, 83% of manufacturers are planning to add North American suppliers to their supply chains within a year, a significant increase from 54% in March 2020.

Thomas' groundbreaking report leverages the platform's unique qualitative and quantitative intelligence on production and sourcing trends through its Industrial Survey Panel and anonymized and aggregated data from Thomasnet.com®’s 1.6 million monthly industrial buyers.

While the report reveals numerous shifts in domestic sourcing trends and supply chain demands, the key takeaway is the industry’s growing prioritization of reshoring in the aftermath of the COVID-19 pandemic.

Potential Economic Impacts of Rising Reshoring Interests in the U.S.

What happens when four in five manufacturers add North American suppliers to their supply chain in the next 12 months?

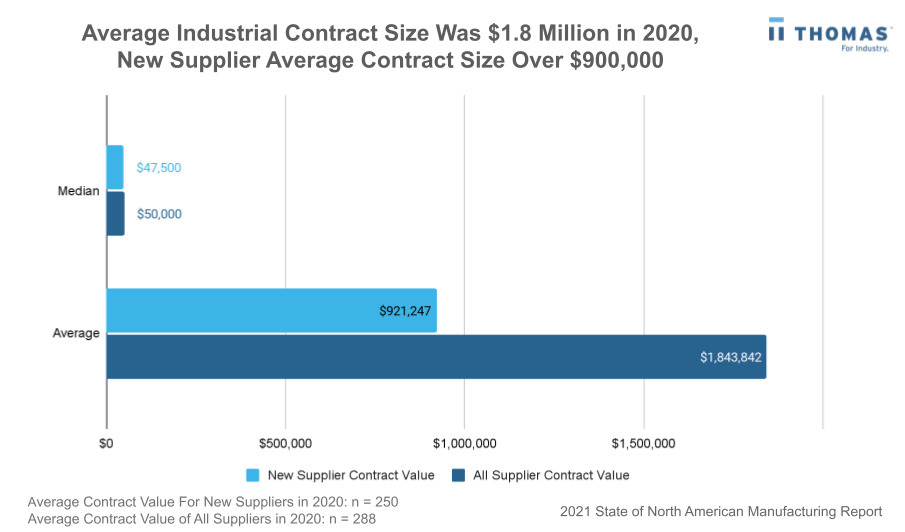

From Thomas' research, manufacturers add an average of 11 suppliers (n=538) to their supply chains on a yearly basis. If 83% of the 579,811 manufacturers in the USA bring on one new supplier (single contract) at an average of $921,247 per contract (n=288), it amounts to a potential $443 billion injection into the U.S. economy.

To understand the potential downstream impacts, let’s look at the types of products and services that are going through a growth spurt for Q1 2021. Thomasnet.com’s year-over-year sourcing data reveal a meaningful increase in demand in Q1 2021 versus 2020 for raw materials, traditional manufacturing services, and advanced manufacturing technologies across key sectors:

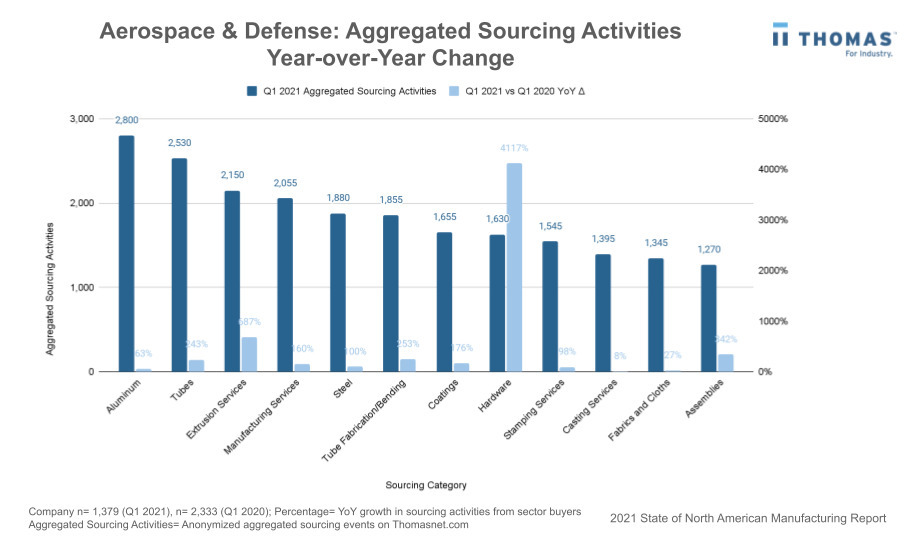

- For raw materials: A surge in demand for aluminum (up by 63% for Aerospace & Defense), steel (up by 92% for Construction), chemicals (up by 142% for Healthcare & Medical), and paper (up by 3,906% for Agriculture).

- For traditional manufacturing output: A 179% growth in sourcing activities for valves and 89% in pumps (Manufacturing).

- For advanced manufacturing technologies, additive manufacturing sourcing activities are up by 4,255% and batteries up by 565% (Automotive).

From Just-in-Time to Availability Optimization

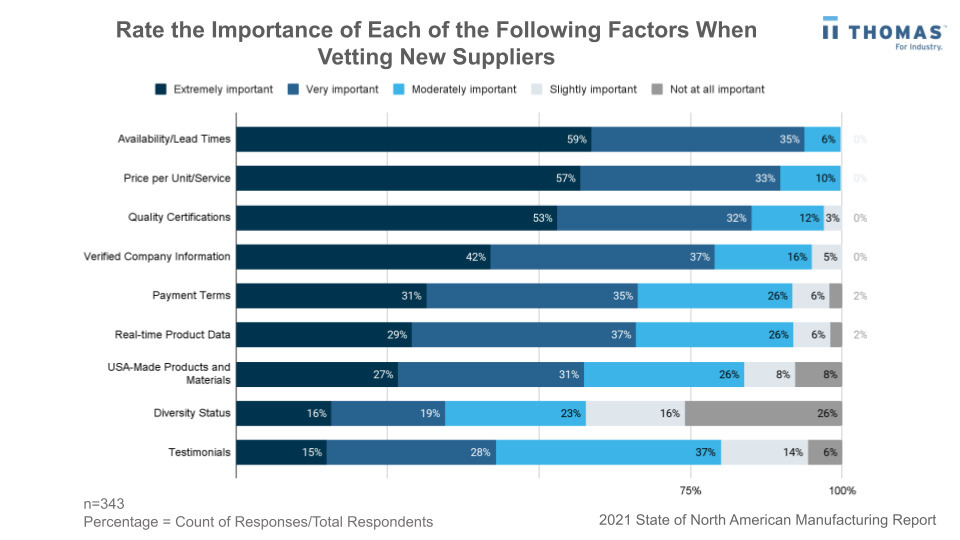

The supply chain disruptions brought on by the pandemic have become a wake-up call for businesses to look beyond cost-saving and just-in-time inventory management. 94% of the manufacturers surveyed listed ‘Availability’ and ‘Lead Times’ as the most important factors when vetting new suppliers, instead of the generally anticipated answer ‘Price per Unit.’ One of our respondents commented, “We need more U.S. manufacturers and the supply chain needs to be strengthened. Just-in-time does not work in a boom.”

If there’s anything positive that came as a result of the intense past year and a half, it’s that many in the industry are calling for more introspection, investment, and support for the wider manufacturing ecosystem and sustainable solutions to future-proof supply chains.

A Different Take on Supplier Relationship Management

In terms of how manufacturers can reap the benefits of the pent-up consumer demand, they can leverage Thomas Industrial Data, as demonstrated by the insights from this report, to stay ahead of supply chain bottlenecks for the fastest-growing sourcing categories across the following key sectors:

- Aerospace & Defense

- Agriculture

- Automotive

- Construction

- Energy & Utilities

- Food & Beverage

- Healthcare & Medical

- Manufacturing

Some of the most notable sourcing category trends that have been observed by sector include:

- Automotive: Additive manufacturing up 4,255% year-over-year (illustrated above)

- Aerospace: Hardware manufacturing up 4,117% year-over-year

- Construction: Lumber (raw materials) up 116% and aluminum up 318%

- Medical and Healthcare: While PPE demand is still leading this sector, compared to last year the sharpest growth is seen on cleaning compounds and chemicals, which are up 2,190%. There is also massive growth in the nutraceutical vertical. Vitamin and supplement manufacturing demand are up by 285% and 350% respectively.

Manufacturers can work on improving product availability and turnaround time for the categories highlighted above, as this is where Thomas forecasts increased spend in North America.

To find out more, download the full 2021 State of North American Manufacturing report.

To look beyond a snapshot of Thomas Industrial Data, you can also contact the Thomas team for more information.

Manufacturing Industry Outlook for 2021 and Beyond

One thing is clear: the pandemic is an impetus for the reframing of manufacturing as a growth machine for North America and an equity driver for our collective future. Manufacturing has the highest multiplier effect of any economic sector, according to Deloitte. For every $1.00 spent in manufacturing, another $2.74 is added to the economy.

Here are two key areas I call for the industry to work together on:

I. Reverse Industry Technical Debt in the USA

The Association of Manufacturing Technology estimated that the United States will need to invest $400-600 billion in manufacturing technologies to improve our trade deficit with our largest importers, such as China. To become competitive, it’s high time the United States increased investment in skilled labor and manufacturing technologies from both operational and technological perspectives.

II. The Future of Our Skilled Labor Force

In collaboration with the Manufacturing Institute, Deloitte released an analysis of the fastest-growing manufacturing occupations for the next decade. It reveals that although it took six years for the manufacturing industry to add 600,000 jobs to the workforce pre-pandemic, the outbreak wiped out a whopping 1.4 million of those jobs. As it stands today, 41% of the jobs have yet to be recovered.

The silver lining of it all is that five out of six of these occupations require a skill set that spans human and technology aspects, and it often does not require formal post-secondary education.

To this end, we can work toward diversity and inclusivity to create environments that promote innovation. 70% of Black professionals surveyed by the Deloitte Diversity, Equity, and Inclusion (DEI) study believe that their company should do more to create a diverse, equitable, and inclusive environment. The Thomas 2020 Women in Manufacturing Benchmark Study shows that only one in three manufacturing professionals and one in four manufacturing leaders are women, although we are half of the population. Studies have shown that bringing together talent with different skill sets and backgrounds is good for business.

Let’s work together to help more talent understand that manufacturing is an incredible career choice, because it really is.

Let’s encourage Gen Z, the makers and the dreamers from all backgrounds, to realize and pursue these exciting opportunities. If you work in the industry and would like to get in touch to chat about this study or share your thoughts, please feel free to reach out to me via LinkedIn or use the ‘Feedback’ tab on this page to say hi. I promise we read all feedback and enjoy hearing from you.

Access the Complete 2021 State of North American Manufacturing Report

Click here to download the full 2021 State of North American Manufacturing report.

You can participate in and receive our future surveys by signing up for the Thomas Industrial Survey Panel.

Report Methodology

The results of the latest State of North American Manufacturing Report are gleaned from two sources:

-

The Thomas Industrial Survey Panel: 709 respondents and 542 responses qualified for our survey facilitated by Thomas via Qualtrics. Participating suppliers were manufacturers from a variety of industrial sectors with revenues spanning from less than $4.9 million to over $500 million.

-

Thomasnet.com Sourcing Activity Data: Sampled and anonymized sourcing data from active industrial buyers by sector on Thomasnet.com between Q1 2020 and Q1 2021 was assembled for this report. Aggregated Sourcing Activities include all behavioral events that indicate the propensity to source, including company profile views, contact initiation activities such as a phone call or click, and a Request for Information (RFI) submission.

Image Credit: Wang An Qi / Shutterstock.com